Non-Applicability of TDS u/s 194O

No TDS if all of the following conditions satisfied: –

- E-commerce participant is individual or HUF;

- Gross amount of sale or service during the previous year is upto ₹ 5 lakhs;

- E-commerce participant have furnished PAN or Aadhar.

Legislative Intent and Context

Section 194O was part of a broader effort [alongside TCS under Section 206C(1H) and others] to ensure tax compliance in digital commerce. Prior to 2020, many small sellers on e-marketplaces fell outside the tax net or underreported income. By placing the onus on established platforms, the government aimed to improve reporting and widen the tax base. In essence, the law mirrors offline TDS (like 194Q on purchase of goods) to the online economy. Over time, authorities have sought to rationalize 194O: for example, the budget for FY 2024-25 cut the TDS rate from 1% to 0.1%, effective from 1/10/2024, to align the burden on online vs offline trade. The stated intent was parity with other thresholds [Section 194Q and Section 206C(1H), both carry 0.1%], thereby reducing compliance strain.

Important Points

- If PAN of e-commerce participant is not available then TDS shall be deducted at 5%.

- Section 194O applies only where the e-commerce participant is a resident of India. If the participant is a non-resident, 194O does not apply (instead, Section 195, equalisation levy or other provisions may govern)

- In case of a transaction to which both section 194O and 194Q (Purchase of goods more than ₹ 50 Lakhs) applies, TDS shall be deducted u/s 194O.

CBDT Clarifications

- 194O does not apply to sales executed on recognized stock exchanges (securities or commodity trades).

- 194O does not apply to e-auction activities such as sale facilitated by OLX. E-auctioneer merely facilitates price discovery on its portal, 194O does not apply since the sale itself is executed off-portal.

- Payment gateway will not be required to deduct TDS u/s 194O, if TDS have been deducted by ECO u/s 194O on the same transaction. E.g. Razorpay not required to deduct TDS u/s 194O if TDS have been deducted by ECO u/s 194O on the same transaction.

- After the first year, an insurance agent or aggregator with no active role in a policy sale need not deduct 194O on commissions earned – instead, the insurance company will deduct TDS on commissions u/s 194H in those subsequent years.

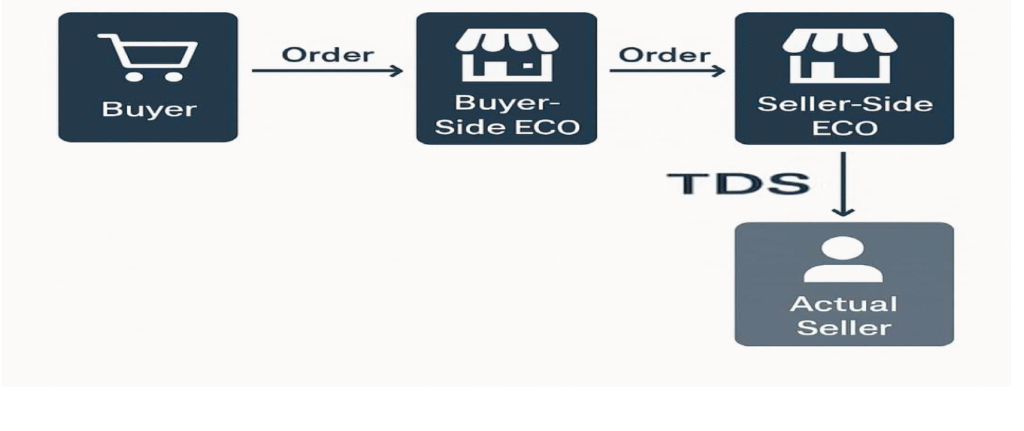

CBDT Guidelines on Open Network for Digital Commerce (ONDC)

If multiple ECO are involved in a transaction, the responsibility for section 194O compliance depends on whether the seller side ECO is the actual seller or not.

Situation 1: If the seller side ECO is not the actual seller, the compliance u/s 194O is to be done by the seller side ECO, who finally releases the payment to the actual seller.

Situation 2: If the seller side ECO is the actual seller, the compliance u/s 194O is to be done by the buyer side ECO, who finally releases the payment to the seller.

{kind=link}